Charles R. Goulding and Preeti Sulibhavi explain how Kone’s blockbuster acquisition of TK Elevator delivers a major private equity payday while quietly setting the stage for expanded use of 3D printing across the global elevator industry.

The elevator industry rarely makes front-page news, but the planned sale of TK Elevator (TKE) to Kone is one of the biggest industrial deals in years. It is not just about consolidation. It is also a story about private equity timing, long-cycle industrial strategy, and the growing role of advanced manufacturing, including 3D printing.

How does Kone’s acquisition of TK Elevator (TKE) impact the R&D and 3D printing landscape?

The acquisition of TK Elevator (TKE) by Kone Corporation for approximately €29.4 billion (US$34.4 billion) creates the world’s largest elevator manufacturer and accelerates the integration of 3D printing (additive manufacturing) into global infrastructure maintenance. This strategic consolidation enables the combined entity to scale Research and Development (R&D) efforts, specifically focusing on obsolete spare parts management, topology optimization for energy efficiency, and digital twin integration through systems like AGILE digital technology. For industrial firms, this transaction underscores the eligibility of advanced manufacturing processes for the Research & Development Tax Credit, particularly regarding wages for technical testing and the cost of filaments consumed during prototyping.

The impact this could have for the industry was obvious to me since I handled the sale of ThyssenKrupp Elevators (TKE) to Dover Corporation for US$1.1 billion, years ago.

What are the Strategic Financial Drivers of the Kone-TKE Deal?

The transaction represents one of the largest private equity exits in European history, following TKE’s 2020 spin-off from Thyssenkrupp.

- Valuation Growth: Private equity firms Advent International and Cinven nearly doubled their valuation from €17 billion in 2020 to the current exit price.

- Operational Synergy: The merger is projected to generate €700 million in annual cost synergies through procurement and R&D consolidation.

- Service Revenue Moat: The deal adds millions of units to Kone’s maintenance portfolio, securing long-cycle service revenue in North and South America.

Finland-based Kone Corporation is one of the world’s leading elevator and escalator companies. It employs more than 60,000 people globally and generates annual revenue in the tens of billions of euros, with a strong focus on service, modernization, and “people flow” systems.

Germany’s TK Elevator, meanwhile, is similarly global in scale. After being spun out of Thyssenkrupp in 2020, it grew into a standalone business with tens of thousands of employees and a particularly strong presence in the Americas.

Together, the two companies would form the world’s largest elevator manufacturer, with combined annual sales of roughly €20 billion and more than 100,000 employees .

That scale matters. Elevators are not just installed once and forgotten. They generate decades of service revenue, and increasingly depend on digital systems, predictive maintenance, and advanced components.

The deal and its structure

The transaction itself is massive. Kone has agreed to acquire TKE for about €29.4 billion (US$34.4 billion), including debt . The deal combines cash, newly issued shares, and assumed liabilities.

It is also historic for another reason: this is one of the largest private equity exits ever in Europe.

TKE has been owned since 2020 by private equity firms Advent International and Cinven, which acquired the business from Thyssenkrupp for about €17 billion. Now, just six years later, they are exiting at nearly double that valuation .

That outcome is significant in today’s market. Private equity firms have struggled to sell large industrial assets due to high interest rates and uncertain capital markets. The TKE sale shows that high-quality industrial businesses can still attract strategic buyers willing to pay a premium.

As the Financial Times noted in its Lex column, the deal highlights how private equity can still “make the elevator pitch work” when the asset is strong and the timing aligns

Private equity’s role: build, hold, exit

Private equity’s involvement in TKE is worth looking at closely.

When Advent and Cinven bought the business in 2020, it was a bold move. The pandemic had just begun, and elevators were suddenly seen as confined spaces to avoid. Financing was leveraged, with significant debt attached to the company.

Instead of aggressively deleveraging, the owners invested in operations and growth. Cash flow was reinvested rather than used to rapidly reduce debt .

That strategy paid off. TKE improved its position in high-margin service and modernization segments, expanded geographically, and strengthened its technology base. By the time of the sale, it had become an attractive strategic target for Kone.

Still, the exit was not straightforward. Private equity had three main options:

- IPO

- Secondary sale to another financial buyer

- Strategic sale to an industry player

An IPO was risky in volatile markets. Another buyout would have required even more leverage. Selling to Kone became the most viable path.

In that sense, this deal reflects a broader shift. Private equity is increasingly dependent on strategic buyers, especially for large industrial assets that require long-term investment and operational expertise.

What are the Strategic Financial Drivers of the Kone-TKE Deal?

From Kone’s perspective, the deal is about scale, geography, and technology.

TKE brings strong positions in North and South America, complementing Kone’s strengths in Europe and Asia. It also adds millions of units under maintenance, which is where much of the industry’s profit is generated.

The transaction represents one of the largest private equity exits in European history, following TKE’s 2020 spin-off from Thyssenkrupp.

- Valuation Growth: Private equity firms Advent International and Cinven nearly doubled their valuation from €17 billion in 2020 to the current exit price.

- Operational Synergy: The merger is projected to generate €700 million in annual cost synergies through procurement and R&D consolidation.

- Service Revenue Moat: The deal adds millions of units to Kone’s maintenance portfolio, securing long-cycle service revenue in North and South America.

But beyond cost savings, there is a deeper reason: modernization.

The global installed base of elevators is aging. Buildings constructed decades ago now require upgrades. These upgrades are increasingly complex, involving digital controls, new materials, and customized components.

That is where additive manufacturing starts to matter.

How is Additive Manufacturing Transforming Elevator Maintenance?

3D printing is transitioning from a prototyping tool to a critical service-line technology within the elevator industry.

| Application Area | Technical Innovation | Industrial Impact |

| Spare Parts | On-demand recreation of obsolete legacy components. | Reduced inventory costs and minimized repair downtime. |

| Sustainability | Topology optimization to reduce component weight. | Improved energy efficiency of vertical transport systems. |

| Prototyping | Rapid testing of customized brackets and housings. | Accelerated innovation cycles without tooling delays. |

Elevator systems are surprisingly complex assemblies. They include structural components, brackets, housings, cable management systems, and customized parts for retrofits.

Traditionally, many of these parts are produced using casting or machining. That works well for large volumes but becomes inefficient for small batches or legacy components.

This is exactly the kind of repair problem 3D printing is designed to solve.

Both Kone and TKE have explored additive manufacturing in recent years, particularly in three areas:

1. Spare parts and obsolescence management

Older elevators often require parts that are no longer manufactured. 3D printing allows these components to be recreated on demand, reducing inventory and repair downtime.

2. Lightweight and optimized components

Additive manufacturing enables topology optimization, reducing weight while maintaining strength. This can improve energy efficiency in elevator systems.

3. Rapid prototyping and product development

New designs can be tested quickly without tooling delays, speeding up innovation cycles.

These applications are not theoretical. Across the broader construction and infrastructure sector, additive manufacturing is already being used for customized parts, structural components, and even large-scale construction elements.

For example, major infrastructure projects such as expansions at ports and logistics hubs increasingly rely on advanced manufacturing techniques to manage complexity and timelines. In projects like the Port Newark expansion in New Jersey, digital construction and advanced fabrication methods are becoming part of the toolkit for large-scale builds .

The service angle: where AM could scale

The most interesting opportunity for 3D printing in the elevator industry is not in new installations. It is in service.

Elevator companies generate a large portion of their revenue from maintaining and upgrading existing systems. This involves:

- Replacing worn components

- Retrofitting systems for new safety standards

- Customizing parts for older buildings

Additive manufacturing can reduce lead times dramatically. Instead of waiting weeks for a part, a service technician could potentially source it locally or have it printed near the installation site.

For a company managing millions of elevators worldwide, even small efficiency gains add up.

This is especially relevant in urban environments where downtime is costly. Hospitals, airports, and high-rise buildings depend on reliable vertical transport.

Private equity meets advanced manufacturing

There is an interesting overlap between private equity strategy and additive manufacturing here.

Private equity firms often focus on operational improvements during their ownership period. These include:

- Supply chain optimization

- Inventory reduction

- Digital transformation

Additive manufacturing fits neatly into this playbook. It can reduce inventory, shorten supply chains, and enable more flexible production.

While there is limited public detail on exactly how extensively TKE deployed 3D printing under private equity ownership, it is reasonable to assume that digital manufacturing initiatives were part of broader efficiency efforts. This includes AGILE digital technology.

Now, under Kone, those efforts could scale further.

What happens next

The deal still faces regulatory scrutiny, particularly in Europe, where antitrust concerns have blocked similar mergers in the past. A previous attempt by Kone to acquire TKE was abandoned due to such concerns .

If approved, the combined company will have the scale to invest heavily in R&D, including digitalization and advanced manufacturing.

For the 3D printing industry, that matters.

Large industrial players are often slow adopters, but when they commit, they deploy at scale. A combined Kone-TKE entity could become a major user of additive manufacturing across its global service network.

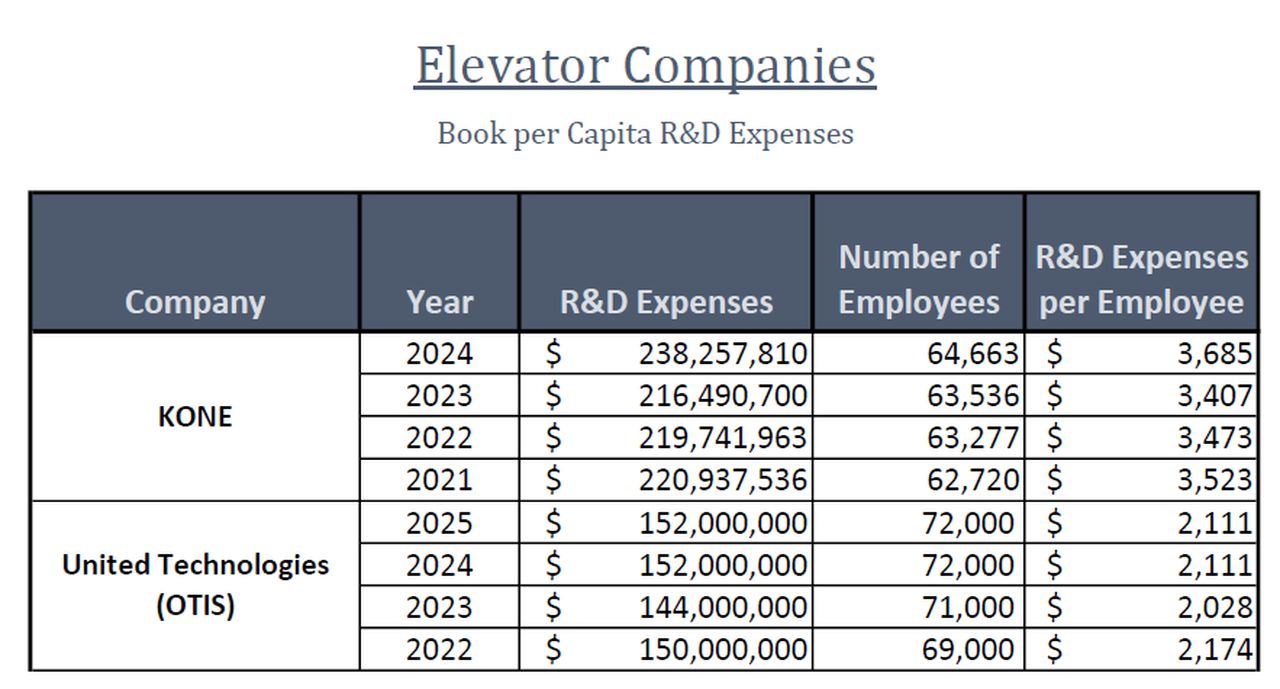

The potential for further research and development (R&D) will only expand with this strategic transaction. Below is a table that presents the R&D spend for two global elevator companies that release their financial information publicly.

How does 3D Printing Qualify for R&D Tax Credits?

Companies utilizing additive manufacturing in the elevator or construction sectors can capture significant tax offsets through the permanent Research & Development Tax Credit.

- Qualified Wages: Wages for technical employees who create, test, and revise 3D-printed prototypes are eligible.

- Process Integration: Time spent integrating 3D printing hardware and software into manufacturing workflows counts as an eligible activity.

- Supplies & Materials: The costs of filaments and raw materials consumed during the development process may be recovered.

- R&D Intensity: 2024 data shows Kone maintains a high R&D intensity, spending US$238,257,810 annually, or US$3,685 per employee.

Whether it is used for creating and testing prototypes or for final production, 3D printing is a strong indicator that R&D-eligible activities are taking place. Companies implementing this technology at any point should consider claiming R&D tax Credits.

Final thoughts

This deal is about more than elevators.

It shows that private equity can still generate strong returns in industrial sectors, even in a challenging market. It highlights the importance of strategic buyers in enabling exits. And it points to a future where advanced manufacturing plays a growing role in maintaining and upgrading the world’s infrastructure.

Elevators may seem mundane, but they sit at the center of urban life. As they become more digital, more connected, and more customized, the technologies used to build and maintain them will evolve as well.

Currently, our firm handles the R&D credits for five of the leading elevator companies currently operating. We see that 3D printing can take a lift with his PE-backed transaction. The industry should pay attention this before the doors close.