Charles R. Goulding and Preeti Sulibhavi explain how manufacturing fundamentals, AI-driven design, and a renewed focus on reliability and workflow integration are defining the industry’s next phase.

At this week’s AMS Strategies Conference in NYC, the tone was pragmatic, not euphoric. The keynote from Yoav Zeif, CEO of Stratasys, didn’t try to gloss over the last few years. Instead, he framed them in context.

And context, he argued, matters.

A Tough Stretch for Additive Manufacturing

Let’s start with the obvious: it’s been a challenging two to three years for additive manufacturing.

Industrial hardware sales have declined year over year when viewed on a quarterly basis. Rising interest rates, geopolitical uncertainty, and general macroeconomic caution slowed capital equipment purchases. Sales cycles lengthened. Customers’ delayed decisions. For many suppliers, 2024 and 2025 were uncomfortable.

Zeif didn’t dispute any of that. In fact, he leaned into it.

Additive manufacturing, he reminded the audience, is fundamentally a capital expenditure business. CAPEX industries are cyclical by nature. Three- to four-year cycles are normal. If you look at semiconductors, machine tools, or other heavy equipment markets, you’ll see similar patterns: investment surges, digestion periods, and then renewed growth.

From that perspective, the last 24 to 36 months look less like structural failure and more like a standard downcycle.

More importantly, he pointed out that the trend line has started to shift. Since Q1 2026, hardware performance has improved. The last two quarters in particular show upward movement. It’s cautious, not explosive, but directionally positive.

If you zoom out, the pattern looks familiar. And that’s the point.

Investment Compresses Time

Zeif opened at a macro level, stepping outside additive manufacturing entirely.

Over the past decade, massive capital investment across advanced technologies has compressed what used to take decades of R&D into just five to eight years. Autonomous vehicles are a prime example. Investment in autonomy didn’t just improve cars. It accelerated lidar, radar, low-latency communications, advanced sensors, AI processing, battery technology, and lightweight materials.

Those advances spill over.

Humanoid robotics. Advanced manufacturing systems. Additive manufacturing. Machine vision. Industrial AI.

Manufacturing technology today is not a collection of isolated silos. It’s an ecosystem.

And at the core of that ecosystem are machine tools.

Machine Tools Still Matter

For all the talk about AI and digital transformation, Zeif grounded the audience with a simple truth: you still have to make things.

Machine tools remain foundational. Without them, nothing moves from design to physical reality. Additive manufacturing is part of that machine tool continuum, not a replacement for it.

When you combine traditional machine tools with emerging technologies such as AI-driven design, advanced materials, robotics, and connected sensors, you’re looking at a multi-trillion-dollar opportunity. Not hype. Infrastructure.

He also emphasized something often overlooked: manufacturing strength is tied to economic strength and national security. A robust manufacturing technology sector is strategic. That matters in today’s geopolitical climate.

In that context, additive manufacturing isn’t a novelty. It’s a strategic capability.

Benchmarking Against Aerospace and Defense

One of the more grounded parts of the keynote was Zeif’s discussion of benchmarking.

If you want to understand where additive manufacturing stands, look at industries that demand performance, certification, and accountability. Aerospace and defense are leading indicators.

These sectors adopt technologies when they are ready, not when they are fashionable.

In aerospace, additive manufacturing has moved well beyond prototyping. It is used for certified flight components, lightweight geometries that cannot be machined conventionally, and low-volume, high-mix production where tooling costs would otherwise be prohibitive.

Defense goes even further. Budgets are larger, urgency is higher, and agility matters. Additive manufacturing enables distributed production, digital inventories, and on-demand part fabrication.

Zeif highlighted what many call “right repair.” Instead of waiting for a spare part to ship across the globe, authorized operators can produce certified replacement components on demand using secure digital files.

That changes logistics.

It reduces downtime.

It shortens supply chains.

It increases resilience.

In defense environments, that resilience is not just a cost issue. It’s a readiness issue. Additive manufacturing supports secure data transmission and localized production, allowing parts to be made where and when they are needed.

The implication is broader than defense. As supply chains remain volatile, industries from energy to transportation can apply similar models. Right to repair, enabled by additive manufacturing, supports distributed manufacturing and reduces dependency on centralized inventory.

That’s a structural advantage, not a short-term sales driver.

Maturing Like CNC Before It

Zeif also addressed a persistent question: why hasn’t additive manufacturing gone mainstream faster?

His answer was historical.

Look at CNC machines. It took roughly 40 years for CNC to become fully mainstream across manufacturing. Early systems were complex. Programming was specialized. CAD integration was limited. Usability barriers were high.

Additive manufacturing is following a similar curve.

The industry must systematically remove friction. That includes better software integration, simpler workflows, automation, material development, and improved reliability. It also means training engineers to design for additive rather than forcing additive into traditional design paradigms.

This is not failure. It’s maturation.

The Low End Is Growing, and That’s Good

Another theme Zeif addressed was the rapid growth of desktop and low-cost 3D printing systems.

In terms of unit volume, low-end systems now surpass industrial machines. Some worry that this fragments the market or commoditizes the technology.

Stratasys sees it differently.

Low-end growth expands awareness. It puts 3D printing into schools, startups, design studios, and small businesses. It creates familiarity. It builds the next generation of engineers who will later specify industrial systems.

Crucially, it does not appear to cannibalize the high end.

Industrial systems compete on reliability, certification, throughput, and workflow integration. Desktop systems compete on accessibility and cost. They serve different use cases. Together, they enlarge the total addressable market.

That dual growth dynamic is healthy.

What the Data Says

Zeif cited annual survey data from roughly 350 additive manufacturing users. The signals are encouraging.

Awareness is rising. Consideration is rising. Usage is rising.

The main friction point remains conversion from consideration to purchase, which is typical in a CAPEX environment.

Perhaps more telling: heavy users plan to increase usage more aggressively than light users. Around 90% of both desktop and industrial users indicate plans to expand usage in 2026.

Satisfaction levels are high, especially among industrial customers. Reliability improvements and enhanced support appear to be paying off.

That’s where the operational story becomes important.

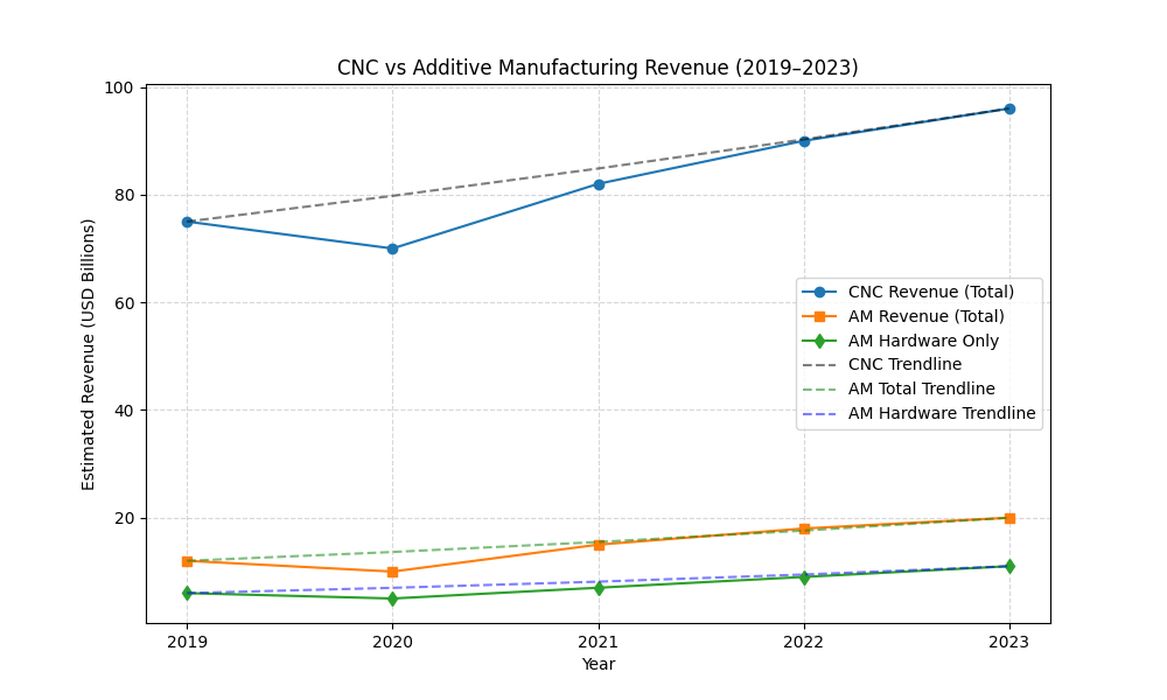

The chart above depicts the position of traditional manufacturing versus AM, in the past few years. However, traditional manufacturing was where AM is now a few decades ago, which means that AM is on the right path, and in the next few decades will be where traditional manufacturing is today.

Hard Work, Measurable Gains

One of the more concrete sections of the keynote focused on execution.

Stratasys worked closely with customers and reported more than a 20% improvement in machine reliability over one year. At a specific customer site, overall equipment efficiency increased from roughly 65% to over 85%.

That’s not marketing language. That’s factory math.

Moving OEE from the mid-60s to the mid-80s transforms additive from an experimental tool into a production asset that can sit alongside traditional equipment.

Zeif emphasized a three-year customer advisory board initiative to gather structured feedback from major corporations. The focus is not on flashy announcements but on practical improvements: reliability, throughput, workflow integration, and software enablement.

In other words, less hype. More plumbing.

AI as the Actuation Layer

AI also made an appearance, but in a grounded way.

As AI accelerates design and concept generation, the bottleneck shifts. It becomes easier to generate ideas and optimized geometries. The constraint moves to physical production.

Additive manufacturing becomes the actuation layer. It turns digital output into physical parts, especially for complex geometries that traditional processes struggle to produce.

This reinforces the long-term positioning of additive manufacturing within the broader manufacturing technology ecosystem.

The Research & Development Tax Credit

The now permanent Research & Development Tax Credit (R&D) is available for companies developing new or improved products, processes, and/or software.

3D printing can help boost a company’s R&D Tax Credits. Wages for technical employees who create, test, and revise 3D printed prototypes can be included as a percentage of eligible time spent for the R&D Tax Credit. Similarly, when used as a method of improving a process, time spent integrating 3D printing hardware and software counts as an eligible activity. Lastly, when used for modeling and preproduction, the costs of filaments consumed during the development process may also be recovered.

Whether it is used for creating and testing prototypes or for final production, 3D printing is a strong indicator that R&D-eligible activities are taking place. Companies implementing this technology at any point should consider claiming R&D tax Credits.

The Right Path

The headline takeaway from Zeif’s keynote was not that additive manufacturing is about to explode overnight.

It was that the industry is behaving exactly as a maturing capital equipment sector should.

Yes, the last two to three years have been difficult.

Yes, hardware sales declined on a quarterly year-over-year basis.

But since Q1 2026, the trend has improved. The last two quarters are moving in the right direction. Usage intent is strong. Satisfaction is high. Aerospace and defense adoption remains robust. Low-end systems are expanding the base. Operational metrics are improving.

When viewed quarter to quarter, the market feels volatile.

When viewed at a macro level, the trajectory is steady.

Three- to four-year cycles are normal in CAPEX industries. Additive manufacturing is no exception.

If Zeif’s charts and arguments are correct, the industry is not in decline. It is in transition, moving from early adopters toward early majority users.

Challenging periods test resilience. They also clarify who is building for the long term.

The message in New York was simple: stay focused, stay practical, and keep improving. The fundamentals, according to both the long-term data and historical patterns, suggest additive manufacturing is on the right path.