There’s a new 3D print industry report from CONTEXT, which now shows entry-level 3D printers as the biggest market segment.

CONTEXT somehow obtains details of company revenues and sales figures, and compiles them into quarterly reports. By examining these reports, it’s possible to understand how the industry is moving from a high-level point of view.

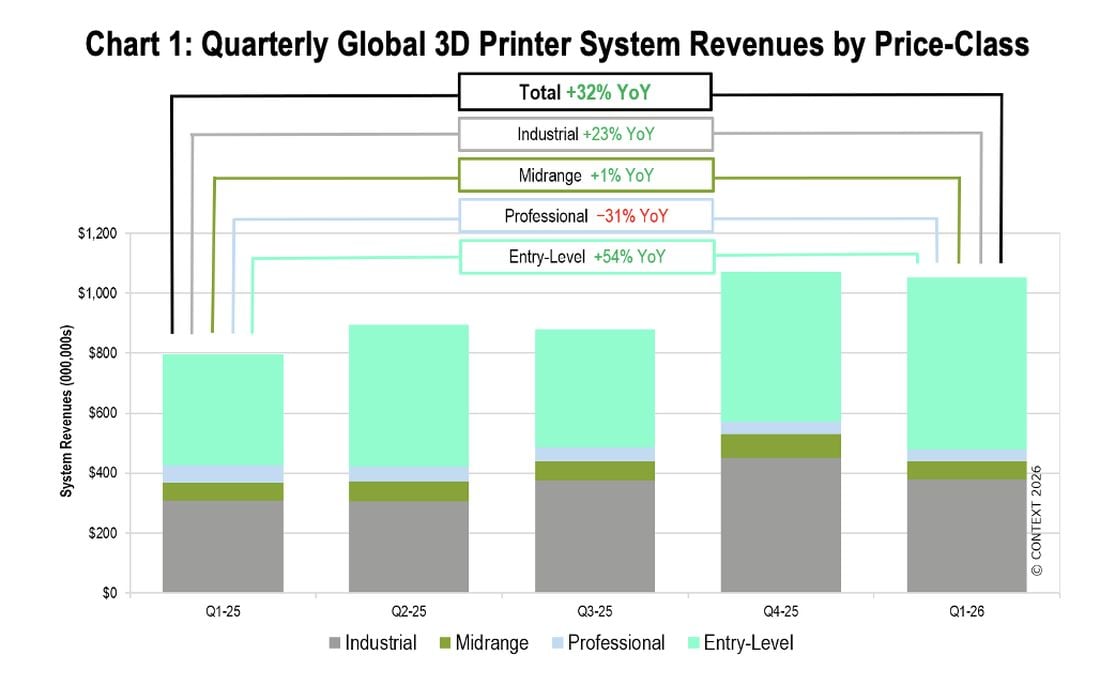

The report splits the market into several major segments:

- Industrial, more than US$100K in price

- Midrange, more than US$20K, but less than US$100K

- Professional, more than US$2.5K

- Entry Level, up to US$2.5K

Overall, CONTEXT reports that the industry in total had revenues grow by a very healthy 32% in the second quarter of this year. However, that growth is absolutely not evenly spread among the different market segments.

The Industrial segment grew 23%, which is quite healthy. This segment includes major metal and polymer systems typically used for manufacturing and regulated industries. There is considerable increased demand in this area, mainly driven by defence applications (drones, especially, it turns out), and smartphone components.

The Midrange segment was flat in this quarter, and the number of shipments actually dropped by six percent. However, they say that the polymer PBF subsegment has grown massively within this category, mainly driven by Formlabs’ new Fuse X1 system and Raise3D’s SLS system. It seems that customers are choosing these lower-cost SLS alternatives over far more expensive industrial SLS solutions.

The Professional segment is the loser in this battle, dropping revenues by 31%. Why such a large drop? It’s because their market is being eaten up by increasingly powerful entry-level equipment: if the US$1,000 machine produces just as good output as the US$25,000 machine, which would you choose? It seems to me that this segment is likely to disappear completely in the next few years, unless someone invents a radically new capability that catches on.

The Entry Level segment grew a whopping 54% this quarter, led by the “Chinese Dragons”, Creality, Bambu Lab, Elegoo, and Anycubic. CONTEXT notes that Flashforge, another Chinese manufacturer, also saw very strong growth in this quarter, likely due to their introduction of new and powerful equipment.

Interestingly, CONTEXT believes that a lot of that entry-level growth is not from sales to individual consumers, but instead from print farms. Large print farms can be set up at a lower cost with squads of entry-level printers and generate high part throughput.

CONTEXT said:

“China has become to the consumer 3D printing market what Japan was to consumer electronics in the 1980s: almost all of the ingenuity, in technical advances like AI and multi-colour printing, and in price innovation, is coming out of China.”

No Western companies were mentioned in the report summary, so you can be sure that any would be far smaller in the market than the leaders. CONTEXT said that the four leading entry-level manufacturers now account for 88% of the revenue in the segment, and that doesn’t even count Flashforge or other Chinese manufacturers. This means that Prusa Research and other prominent Western entry-level 3D printer manufacturers must now be less than five percent of the market.

Via CONTEXT