Charles R. Goulding and Andressa Bonafe examine how Johnson & Johnson’s spin-off of DePuy Synthes sets the stage for a more agile, 3D printing–driven orthopaedics powerhouse ready to redefine surgical innovation.

On October 14, 2025, Johnson & Johnson announced its intent to separate its orthopaedics unit into a stand-alone company, DePuy Synthes, on an 18 to 24 month timetable. The orthopaedics business, maker of hip, knee and shoulder implants plus related instruments, generated about US$9.2 billion in 2024, roughly ten percent of J&J’s revenue, but has grown more slowly and at lower margins than other device categories, according to the company’s CFO Joe Wolk. The spin-off will make DePuy Synthes the largest orthopaedics-focused company globally, while allowing the remaining J&J MedTech and Innovative Medicine portfolio to concentrate capital where the pace of innovation and earnings is higher.

Strategically, this is the next chapter in J&J’s simplification playbook that began with the divestiture of Kenvue, the consumer health company, in 2023. It also unwinds part of a decades-long orthopaedics build-out, most notably the 21 billion-dollar Synthes acquisition of 2012, folded into DePuy, which J&J originally bought in 1998. Leadership for the transition will come from Namal Nawana, appointed worldwide president of DePuy Synthes.

The competitive backdrop matters. Specialized rivals have been pressing hard: Ottobock’s 4.2 billion euro Frankfurt IPO on October 9, 2025, highlighted investor appetite for focused ortho-tech platforms, while players like Stryker and Zimmer Biomet continue to scale. In this context, J&J’s split is less a retreat than a portfolio sharpening, and, crucially for additive-manufacturing, a setup that could accelerate orthopaedics’ shift to digital planning and 3D printed, patient-specific solutions under a nimbler, specialty-only structure.

Inside DePuy Synthes’ Additive Portfolio

Few orthopaedics manufacturers have embraced additive manufacturing as systematically as DePuy Synthes. Over the past decade, Johnson & Johnson’s orthopaedics division has turned 3D printing from a design curiosity into a clinical production method that now underpins several of its key implant families and digital-surgery workflows. The company built internal capability through its 3D Printing Center of Excellence, which has accelerated instrument design, custom implants, and rapid prototyping across J&J MedTech. It also expanded through acquisition and partnership, acquiring Emerging Implant Technologies (EIT) in 2018 to bring in-house the lattice-structured titanium used in spinal cages, and partnering with Materialise to integrate patient-specific cranio-maxillofacial (CMF) solutions into its TRUMATCH portfolio. Collaborations with HP Inc. have explored how distributed 3D printing and digital design can personalize instruments and surgical components closer to the point of care.

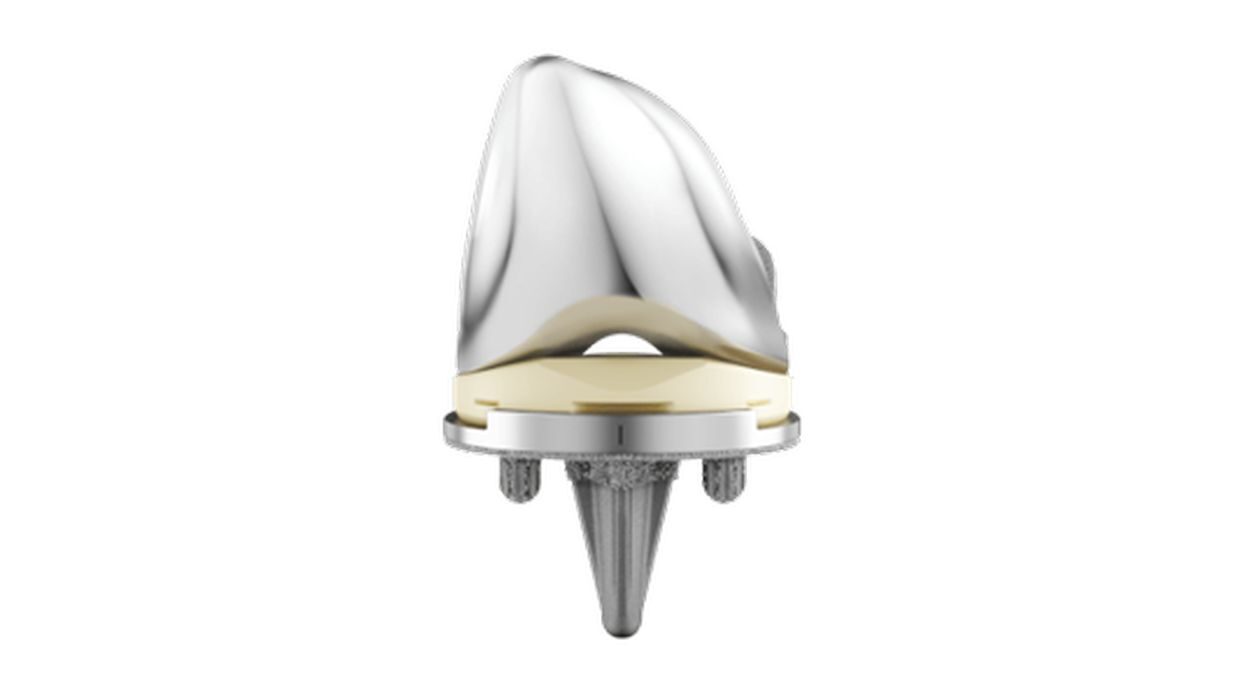

Within DePuy Synthes’ product line, 3D printing already anchors multiple high-visibility systems:

• TRUMATCH™ CMF: patient-specific titanium plates, implants, and surgical guides produced from CT data for cranio-maxillofacial reconstruction.

CONDUIT™ Interbody Platform: spinal implants printed in porous titanium with cellular architecture designed to mimic bone and enhance fusion.

ATTUNE™ AFFIXIUM™ Knee: cementless knee components using a 3D printed lattice structure that promotes bone ingrowth and initial stability.

These examples show a consistent design language: porous, biomimetic structures, patient-specific geometries, and digitally connected surgical planning that differentiates DePuy Synthes from conventional implant producers. In practical terms, that means that the orthopaedics division already operates within a hybrid model, with high-volume printed components for spine and knee and on-demand patient-specific implants for trauma and CMF.

For J&J, 3D printing has become a bridge between engineering precision and surgical personalization. For DePuy Synthes, about to stand on its own, those same capabilities now represent a potential growth engine, ready to scale once the company can focus exclusively on orthopaedics without competing for capital across J&J’s broader MedTech portfolio.

Perspectives for the Future

The spin-off arrives at a moment when orthopaedics is separating into two categories. On one side stand the specialized innovators, such as Ottobock, Stryker, Zimmer Biomet, and an expanding field of smaller additive-enabled startups such as Open Bionics and 3D Systems Healthcare. On the other is a shrinking group of diversified medical-device conglomerates whose capital must compete across cardiovascular, surgical, and vision segments. By creating a stand-alone DePuy Synthes, Johnson & Johnson is deliberately shifting from the second camp to the first.

Freed from the budgeting cycles and portfolio trade-offs of a global healthcare giant, DePuy Synthes can act more like a focused orthopaedics technology company: faster in product development, closer to surgeons, and able to channel investment directly into additive platforms. The business already commands roughly US$9 billion in annual sales, a base large enough to scale new production methods but narrow enough to prioritize them.

Operational independence could widen the scope of innovation. A leaner DePuy Synthes could deploy additive manufacturing to shorten supply chains, localize production near hospitals, and expand the use of digital surgical planning linked to on-demand printing. With maturing regulations and improving titanium and polymer economics, the barriers to shifting from pilots to mainstream production are markedly lower.

Competitively, this move positions DePuy Synthes to counter Ottobock’s post-IPO momentum and to challenge Stryker’s and Zimmer Biomet’s robotics-plus-implant ecosystems with its own digitally native, additive-driven platform. In that sense, the separation is not a retreat but a reset. It transforms J&J’s century-old orthopaedics business into one that can move at start-up speed within a Fortune-size infrastructure.

For U.S.-based orthopaedics companies, the ongoing expansion of 3D printing in product development, materials testing, and process automation creates a clear opportunity to leverage federal and state Research & Development Tax Credits. As DePuy Synthes and its peers scale additive programs, the technical work behind those improvements qualifies as R&D under U.S. tax law. In practice, that means companies investing in innovation can recover a portion of their costs while advancing the next generation of patient-specific implants.

The Research & Development Tax Credit

The now permanent Research and Development (R&D) Tax Credit is available for companies developing new or improved products, processes and/or software.

3D printing can help boost a company’s R&D Tax Credits. Wages for technical employees creating, testing and revising 3D printed prototypes can be included as a percentage of eligible time spent for the R&D Tax Credit. Similarly, when used as a method of improving a process, time spent integrating 3D printing hardware and software counts as an eligible activity. Lastly, when used for modeling and preproduction, the costs of filaments consumed during the development process may also be recovered.

Whether it is used for creating and testing prototypes or for final production, 3D printing is a great indicator that R&D Credit eligible activities are taking place. Companies implementing this technology at any point should consider taking advantage of R&D Tax Credits.

Conclusion

The planned separation of DePuy Synthes marks more than a corporate restructuring. It represents a strategic shift toward speed, specialization, and the kind of digital manufacturing that is reshaping orthopaedics worldwide. As 3D printing matures from pilot projects to large-scale production, the new company will have the autonomy to direct capital and talent toward technologies that shorten design cycles, localize production, and bring surgical customization closer to patients.

For Johnson & Johnson, the spin-off continues a broader evolution toward higher-growth, higher-margin segments in medicine and devices. For the U.S. orthopaedics sector, it highlights how additive manufacturing and supportive R&D incentives can reinforce one another, turning technical innovation into both competitive advantage and measurable economic value. If DePuy Synthes succeeds, it may set the template for how established MedTech brands reinvent themselves for the additive age.