Charles G. Goulding explains how the convergence of AI data center energy demands and advanced nuclear engineering has turned additive manufacturing into a critical pathway for securing lucrative Federal R&D Tax Credits.

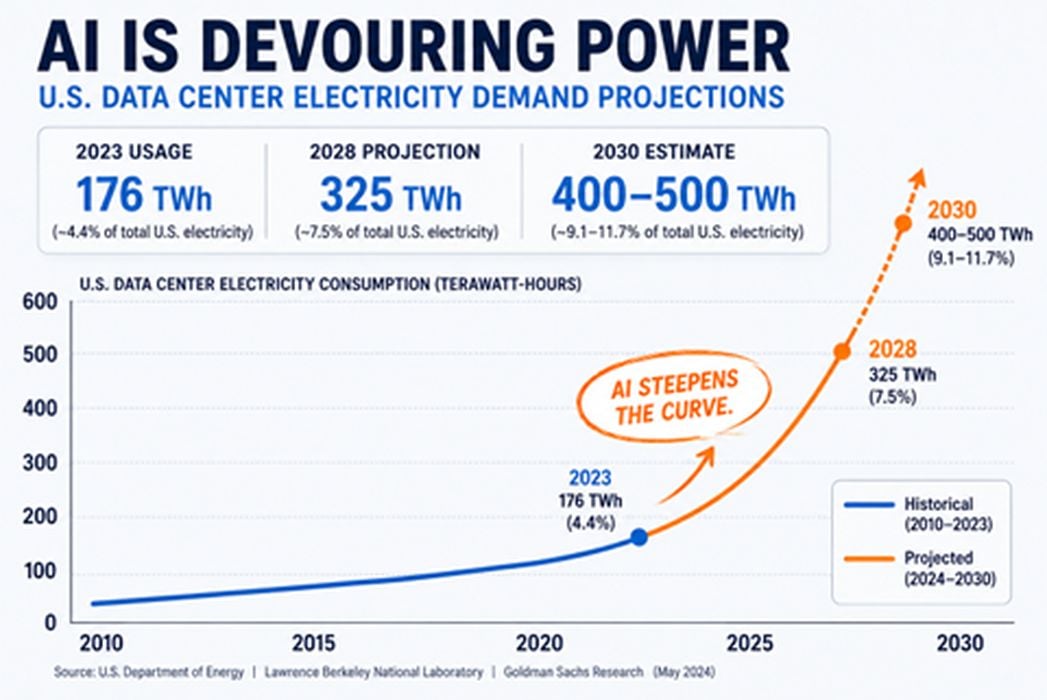

The amount of energy required to power the AI buildout is enormous — and rising fast. New AI models, hyperscale data centers, and advanced compute infrastructure are driving electricity demand upward at a pace the existing grid was never designed to handle.

That reality is rapidly pushing nuclear energy back toward the center of infrastructure planning. Once viewed as too expensive, too slow, or politically untouchable, nuclear power is increasingly being reconsidered as one of the few scalable sources capable of delivering the constant, around-the-clock electricity that AI infrastructure requires.

But designing advanced reactors is only part of the challenge. Building them fast enough may be even harder.

Critical reactor components, cooling systems, transformers, and specialized industrial parts often face severe supply-chain bottlenecks and manufacturing delays measured in years, not months. To help accelerate deployment, the U.S. Department of Energy is now considering billions of dollars in support for nuclear supply chains, long-lead component manufacturing, and advanced production capabilities.

That focus on long-lead bottlenecks may create a significant opportunity for additive manufacturing.

The Power Crunch

The explosion of AI models, giant data centers, and nonstop computing growth all carry intense energy requirements. AI has quickly become the biggest driver of new electricity demand in the modern economy. And the curve keeps steepening.

The existing grid in the US was never designed to handle this type of demand. Without enough reliable power and faster deployment timelines, however, AI infrastructure cannot come online as quickly as it otherwise needs to.

China appears to have done a better job anticipating its new energy needs. Indeed, China has spent years expanding generation capacity in line with the emergence of new data centers and compute hubs. The United States is now racing to do the same.

In this sense, the energy demand problem is also a national security problem. That explains why Washington is suddenly focused on long-lead bottlenecks, domestic production capacity, advanced nuclear deployment, and technologies capable of accelerating the AI buildout.

The AI Power Crunch and the Shift to Decentralized Nuclear Energy

Why is AI Infrastructure Driving Nuclear Energy Demand?

Not long ago, nuclear energy was widely viewed as politically toxic, too expensive, or simply out of fashion.

Now it is back at the center of long-term national planning.

Instead of giant centralized reactors tied to sprawling grid systems, many companies are now pursuing smaller, more modular designs. The rapid expansion of advanced compute infrastructure, hyperscale data centers, and complex AI models has made AI the fastest-growing driver of electricity demand in the modern economy. Because AI infrastructure requires an uninterrupted, constant baseload supply of power to maintain continuous operation, intermittent renewable energy sources are often insufficient.

Consequently, energy planners are turning to advanced nuclear energy as a scalable, weather-independent alternative. While global competitors like China have systematically expanded generation capacity over several years to align with emerging compute hubs, the United States is currently accelerating domestic production capacity to address what has evolved into a critical

What is the Role of Small Modular Reactors (SMRs) and Microreactors?

To deploy power rapidly and eliminate regional grid transmission bottlenecks, the nuclear industry is transitioning to decentralized, compact reactor designs. These systems include:

- Small Modular Reactors (SMRs): Factory-built, scalable nuclear systems designed for rapid deployment.

- Microreactors: Compact, highly flexible power systems built directly adjacent to the end-user.

Part of the appeal is decentralization. Older reactors connect to huge regional grids. By contrast, compact reactors sit beside places where electricity is consumed.

Microreactor Industry Case Study: Oklo Inc. Microreactors

* Industry: Advanced Nuclear Power Generation / AI Compute Infrastructure

* Innovation: In 2024, Meta partnered with advanced nuclear developer Oklo Inc. to deploy localized, compact Aurora microreactors. These reactors provide dedicated, resilient, and independent 24/7 power with a minimal physical footprint.

* Impact: Operational testing of the Aurora reactor is scheduled at the Idaho National Laboratory by 2028, with localized commercial power delivery to Meta’s computing hub in Pike County, Ohio, finalized by 2030.

In 2024, Meta announced partnerships with advanced nuclear developers for localized power generation at its hub in Pike County, Ohio. One of Meta’s chosen partners is Oklo, a designer of compact microreactors. Unlike traditional nuclear plants, Oklo’s Aurora reactors are intended to be smaller, modular, and more flexible. Their reactors sit directly next to AI campuses, data centers, military installations, and industrial hubs for dedicated power with a smaller physical footprint.

For companies racing to build energy-hungry AI infrastructure, Oklo’s combination of localized deployment, resiliency, and nonstop power generation has made microreactors a closely watched subject.

“AI is reshaping the energy landscape,” Oklo CEO Jacob DeWitte said following the Meta announcement. “Advanced nuclear can provide reliable, scalable power directly where it is needed most.”

By 2028, Oklo plans to test its Aurora reactor at Idaho National Laboratory, with power then planned for delivery to Meta in Pike County, Ohio by 2030.

Overcoming Nuclear Supply Chain Bottlenecks with Additive Manufacturing

How Does 3D Printing Unclog Long-Lead Component Choke Points?

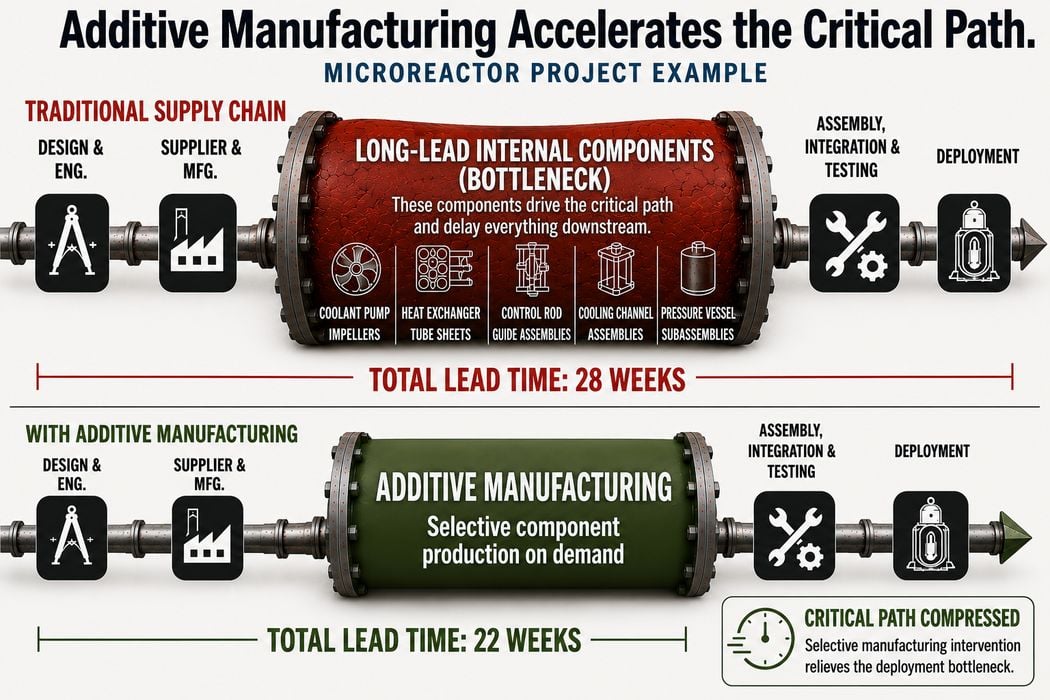

Moving toward thousands of localized microreactors creates severe logistical challenges, where a few delayed, long-lead components can stall an entire infrastructure project. Traditional manufacturing methods for specialized internal reactor components frequently face supply-chain bottlenecks measured in years.

Additive manufacturing (3D printing) resolves these critical-path constraints by completely eliminating tooling requirements, streamlining complex designs, and consolidating multipart assemblies into singular structural components. Furthermore, it transitions infrastructure logistics from physical warehousing to a model of digital inventory, where rare printable part files are stored securely and manufactured on demand directly near the deployment site.

Leading institutions and market players driving this advanced integration include:

- Westinghouse Electric Company: Actively fabricating and installing operational 3D printed nuclear components.

- Oak Ridge National Laboratory (ORNL): Dedicated to the multi-year development of additive manufacturing processes engineered specifically for advanced reactor systems.

- GE Additive: Operating at the precise cross-section of high-specification industrial turbines, aerospace-grade materials, and advanced energy applications.

Critical Reactor Choke Points Resolved by Additive Manufacturing

| Component Choke Point | Traditional Supply Chain Impact | Additive Manufacturing Solution |

| Coolant Pump Impellers | Multi-month delays due to complex cast tooling requirements. | Direct printing from digital files without tooling. |

| Heat Exchanger Tube Sheets | Intense machining hours and high material waste. | Near-net-shape printing with consolidated structures. |

| Flow-Control Assemblies | Multi-part structural joints prone to structural failure. | Monolithic part consolidation eliminating joints. |

| Cooling-Channel Structures | Geometrical limitations under subtractive machining. | Complex, high-performance internal geometries. |

Several 3D printing companies have moved into this space. Westinghouse Electric Company has produced and installed 3D printed nuclear components, while Oak Ridge National Laboratory (ORNL) has spent years developing additive manufacturing processes tied to advanced reactor systems and high-performance energy applications.

Industrial players like GE Additive are also positioned at the intersection of energy systems, aerospace-grade materials, turbine technologies, and high-specification industrial production.

3D printing may also fundamentally change how companies think about inventory itself. Instead of warehousing rare components for years, future distributed energy systems may increasingly rely on digital inventories — printable part files that can be produced on demand closer to deployment sites.

Will 3D Printing Support Space-Based Orbital Data Centers?

As AI data demands expand beyond earthbound limitations, aerospace entities like SpaceX and Axiom Space are actively evaluating orbital data infrastructure and autonomous space-based energy systems. Because physical supply lines cannot support a six-month delivery window for replacement parts in orbit, space-bound infrastructure will rely fundamentally on autonomous, robotic 3D printers. These systems will print critical tools, cooling components, and structural elements on demand directly in space.

Recent discussions around orbital computing and space-based data infrastructure have pushed concepts that once sounded like science fiction into mainstream conversation.

The basic idea is straightforward: giant computing centers operate in orbit, powered by advanced energy systems and maintained by autonomous machines.

“The future data center may not be earthbound,” one aerospace executive recently remarked during discussions surrounding orbital compute infrastructure. “As AI scales, computing itself may eventually migrate toward wherever energy and cooling are most efficient.”

Once those systems leave Earth, however, logistics become radically harder. Replacement parts cannot take six months to arrive from suppliers halfway across the planet.

Orbital systems may therefore rely on robotic 3D printers capable of producing replacement parts, tools, structural components, and cooling systems directly in space.

As computing systems become more decentralized, autonomous, and modular, additive manufacturing may become one of the core technologies tying all of it together.

How Does 3D Printing Accelerate the R&D Tax Credit for Nuclear Component Manufacturing?

The Federal Research and Development (R&D) Tax Credit (Internal Revenue Code Section 41) offers a direct dollar-for-dollar tax offset—typically ranging from 4% to 7% of eligible expenditures—for domestic companies utilizing additive manufacturing (3D printing) to produce advanced nuclear reactor component parts. As massive data center buildouts for Artificial Intelligence (AI) drive unprecedented demand for continuous, 24/7 electricity, the nuclear sector is shifting away from massive, centralized regional grids toward decentralized, localized power systems like Small Modular Reactors (SMRs) and microreactors. Additive manufacturing systematically compresses the traditional 28-week manufacturing critical path down to 22 weeks by bypassing long-lead supply chain bottlenecks for highly specialized internal components. Under the PATH Act, eligible companies can use these credits to offset the Alternative Minimum Tax (AMT) or claim up to US$500,000 annually against federal payroll taxes for qualified startup businesses.

Qualifying for the Section 41 R&D Tax Credit

The Four-Part Statutory Test for Additive Nuclear Manufacturing

To qualify expenditures for the Federal R&D Tax Credit, the design, development, and testing of 3D printed nuclear components must satisfy the IRS Four-Part Test:

- Permitted Purpose (Section 41(d)(1)(B)): The activity must relate to developing or improving the reliability, performance, quality, or functional capability of a business component (e.g., maximizing the thermal efficiency of a 3D printed heat exchanger).

- Elimination of Uncertainty (Section 41(d)(1)(A)): The taxpayer must encounter technical uncertainty regarding the capability, methodology, or final optimal design of the component at the project’s inception.

- Process of Experimentation (Section 41(d)(1)(C)): The company must systematically evaluate alternative designs or parameters through modeling, simulation, pre-production testing, or iterative 3D printing runs to resolve the technical uncertainty.

- Technological in Nature (Section 41(d)(1)): The process of experimentation must fundamentally rely on principles of physical science, biological science, engineering, or computer science.

What Expenditures are Eligible for R&D Tax Relief?

Companies engaging in additive manufacturing for nuclear applications can claim Qualified Research Expenses (QREs) across several major categories:

- Wages: W-2 taxable wages paid to domestic engineers, 3D printing technicians, metallurgists, and software developers directly executing or supervising the R&D process.

- Supplies: The direct costs of raw materials consumed during the experimental printing process, including high-grade metal powders (e.g., Inconel, titanium alloys) and specialized industrial substrates used in pre-production testing.

- Contract Research: Incurred expenses paid to eligible domestic third-party contractors, such as testing labs performing destructive or non-destructive evaluations on 3D printed parts.

- Patent Costs: Legal and administrative expenditures directly associated with filing and securing patents for the newly developed additive manufacturing processes or unique component designs.

The Race to Build

Even if data centers never make it to space, decentralization is clearly a key trend moving forward. Instead of a handful of giant centralized facilities tied to sprawling grids, the future looks like localized hubs paired with localized energy — including microreactors and other compact nuclear systems.

In that world, the chokepoints matter as much as technologies themselves.

That is why Washington is suddenly focused on long-lead nuclear supply chains, why companies like Meta are partnering with firms like Oklo, and why additive manufacturing is attracting so much attention. The opportunity may not be to reinvent industry from scratch, but to help unclog the critical pathways slowing the next generation of energy and AI infrastructure from coming online.

Charles G. Goulding is a practicing attorney.